UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

Proxy Statement Pursuant to Section 14(a) of the Securities

Exchange Act of 1934 (Amendment No.)

Filed by the Registrant x

Filed by a Party other than the Registrant o

Check the appropriate box:

| [ | Preliminary Proxy Statement. |

| [ ] | Confidential, for use of the Commission Only (as permitted by Rule 14a-6(e)(2)). |

| [ | Definitive Proxy Statement. |

| [ ] | Definitive Additional Materials. |

| [ ] | Soliciting Material Pursuant to § 240.14a-12. |

ETF SERIES SOLUTIONS

| (Name of Registrant as Specified In Its Charter) |

(Name of Person(s) Filing Proxy Statement, if other than the Registrant)

Payment of Filing Fee (Check the appropriate box):

x No fee required.

o Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11.

| (1) Title of each class of securities to which transaction applies: |

| (2) Aggregate number of securities to which transaction applies: |

| (3) Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): |

| (4) Proposed maximum aggregate value of transaction: |

| (5) Total fee paid: |

o Fee paid previously with preliminary materials:

o Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing.

| (1) Amount Previously Paid: |

| (2) Form, Schedule or Registration Statement No.: |

| (3) Filing Party: |

| (4) Date Filed: |

each a series of ETF Series Solutions

615 East Michigan Street, Milwaukee, Wisconsin 53202

Dear Shareholder:

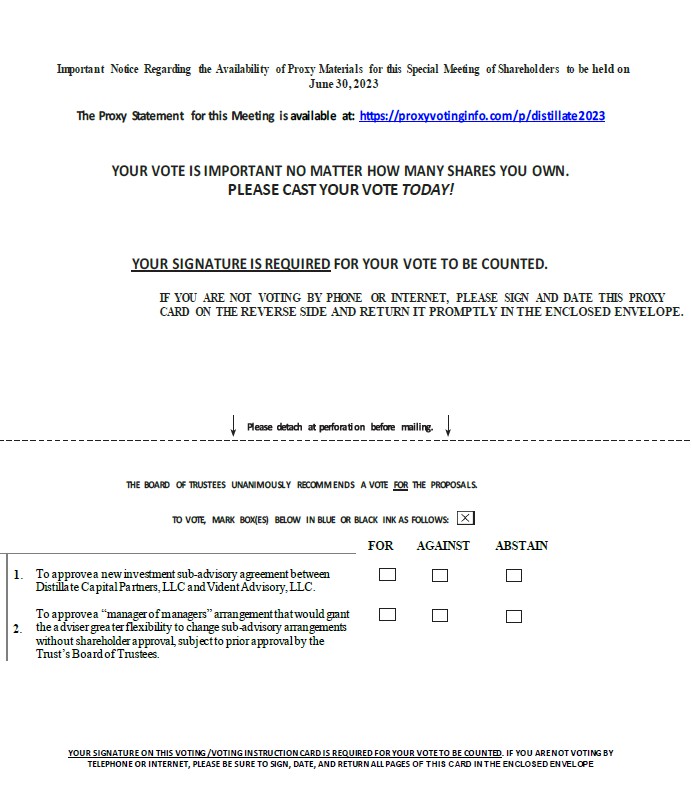

I am writing to inform you about an upcoming special meeting (the “Special Meeting”) of the shareholders of the VidentDistillate Small/Mid Cash Flow ETF, Distillate U.S. Bond Strategy ETF™, Vident U.S. Equity Strategy ETF™, VidentFundamental Stability & Value ETF, and Distillate International Equity Strategy ETF™, and U.S. Diversified Real EstateFundamental Stability & Value ETF (each, a “Fund,”“Fund” and, collectively, the “Funds”), each a series of ETF Series Solutions (the “Trust”). The Special Meeting is being held to seek shareholder approval of the Proposal (thefollowing Proposals (each, a “Proposal” and, together, the “Proposals”) discussed below and in the accompanying Proxy Statement:

PROPOSAL 1: For shareholders of each PROPOSAL 2: For shareholders of each Fund, separately, to approve a “manager of managers” arrangement that would grant the applicable Fund and the Adviser greater flexibility to change sub-advisory arrangements without shareholder approval, subject to prior approval by the Trust’s Board of Trustees. No increase in shareholder fees or expenses is being proposed. |

Enclosed you will find a notice of the Special Meeting, a Proxy Statement with additional information about the Proposal,Proposals, and a proxy card with instructions for voting. Following this letter, you will find questions and answers regarding the Proxy Statement that are designed to help you understand the Proxy Statement and how to cast your votes. These questions and answers are being provided as a supplement to, not a substitute for, the Proxy Statement, which we urge you to review carefully.

The Board of Trustees of the Trust believes that the Proposal isProposals are in the best interest of the relevant Fund(s)Funds and itstheir shareholders and recommends that you vote “FOR” the relevant Proposal.Proposals. Importantly, approval of the ProposalProposals will not result in any increase in shareholder fees or expenses.

The Special Meeting is scheduled to be held at 11:00[TIME] a.m. Central time on June 9,30, 2023, at the offices of U.S. Bank Global Fund Services, 615 East Michigan Street, Milwaukee, Wisconsin 53202. If you are a shareholder of record as of the close of business on May 9,15, 2023, you are entitled to vote at the Special Meeting and at any adjournment thereof. Your vote is extremely important. While you are welcome to join us at the Special Meeting, most shareholders will cast their votes by filling out, signing, and returning the enclosed proxy card, voting by telephone, or voting using the internet.

We intend to hold the Special Meeting in person. However, we are sensitive to the public health and travel concerns our shareholders may have and recommendations that public health officials may issue in light of the evolving COVID-19 pandemic. As a result, we may impose additional procedures or limitations on Special Meeting attendees or may decide to hold the Special Meeting in a different location or solely by means of remote communication. We plan to announce any such updates on our proxy website www.videntam.com,https://proxyvotinginfo.com/p/distillate2023, and we encourage you to check this website prior to the Special Meeting if you plan to attend. We also encourage you to consider your options to vote by internet, telephone, or mail, as discussed in the enclosed proxy card, in advance of the Special Meeting in the event that, as of June 9,30, 2023, in-person attendance atthe Special Meeting is either prohibited under a federal, state, or local order or contrary to the advice of public health care officials.

If you have any questions regarding the ProposalProposals or Proxy Statement, please do not hesitate to call toll-free 866-839-1852.[866-839-1852]. Representatives will be available Monday through Friday, 9 a.m. to 10 p.m. Eastern time. Thank you for taking the time to consider these important ProposalProposals and for your continuing investment in the Fund(s).

Sincerely,

Joshua J. Hinderliter

Secretary

ETF Series Solutions

DISTILLATE SMALL/MID CASH FLOW ETF (DSMC)

each a series of ETF Series Solutions

615 East Michigan Street, Milwaukee, Wisconsin 53202

NOTICE OF SPECIAL MEETING

TO BE HELD ON JUNE 9,30, 2023

A special meeting of shareholders (the “Special Meeting”) of the VidentDistillate Small/Mid Cash Flow ETF, Distillate U.S. Bond Strategy ETF™, Vident U.S. Equity Strategy ETF™, VidentFundamental Stability & Value ETF, and Distillate International Equity Strategy ETF™, and U.S. Diversified Real EstateFundamental Stability & Value ETF (each, a “Fund,”“Fund” and, collectively, the “Funds”), each a series of ETF Series Solutions (the “Trust”), will be held at 11:00[ ] a.m. Central time on June 9,30, 2023, at the offices of U.S. Bank Global Fund Services, 615 East Michigan Street, Milwaukee, Wisconsin 53202. At the Special Meeting, shareholders of the Funds will be asked to act upon the following Proposal:Proposals:

PROPOSAL 1: For shareholders of each PROPOSAL 2: For shareholders of each Fund, separately, to approve a “manager of managers” arrangement that would grant the applicable Fund and the Adviser greater flexibility to change sub-advisory arrangements without shareholder approval, subject to prior approval by the Trust’s Board of Trustees. No increase in shareholder fees or expenses is being proposed. |

THE BOARD OF TRUSTEES, INCLUDING ALL OF THE INDEPENDENT TRUSTEES,

RECOMMENDS THAT YOU VOTE “FOR” THEPROPOSAL.PROPOSALS.

RECOMMENDS THAT YOU VOTE “FOR” THE

The Trust’s Board of Trustees has fixed the close of business on May 9,15, 2023, as the Record Date for the determination of the shareholders entitled to notice of, and to vote at, the Special Meeting and any adjournments thereof.

Please read the accompanying Proxy Statement. Your vote is very important to us regardless of the number of shares you hold. Shareholders who do not expect to attend the Special Meeting are requested to complete, sign, and promptly return the enclosed proxy card so that a quorum will be present, and a maximum number of shares may be voted for the applicable Fund. In the alternative, please call the toll-free number on your proxy card to vote by telephone or go to the website shown on your proxy card to vote over the internet. Proxies may be revoked prior to the Special Meeting by giving written notice of such revocation to the Secretary of the Trust prior to the Special Meeting, delivering a subsequently dated proxy card by any of the methods described above, or by voting in person at the Special Meeting.

We intend to hold the Special Meeting in person. However, we are sensitive to the public health and travel concerns our shareholders may have and recommendations that public health officials may issue in light of the evolving COVID-19 pandemic. As a result, we may impose additional procedures or limitations on Special Meeting attendees or may decide to hold the Special Meeting in a different location or solely by means of remote communication. We plan to announce any such updates on our proxy website www.videntam.com,https://proxyvotinginfo.com/p/distillate2023, and we encourage you to check this website prior to the Special Meeting if you plan to attend. We also encourage you to consider your options to vote by internet, telephone, or mail, as discussed in the enclosed proxy card, in advance of the Special Meeting in the event that, as of June 9,30, 2023, in-person attendance atthe Special Meeting is either prohibited under a federal, state, or local order or contrary to the advice of public health care officials.

By Order of the Board of Trustees

Joshua J. Hinderliter

Secretary

ETF Series Solutions

IMPORTANT INFORMATION TO HELP YOU UNDERSTAND THE PROPOSALPROPOSALS

Below is a brief overview of the mattermatters being submitted to a shareholder vote at the special meeting of shareholders (the “Special Meeting”) to be held on June 9,30, 2023. Your vote is important, no matter how large or small your holdings may be. Please read the full text of the proxy statement (“Proxy Statement”), which contains additional information about the proposal (theproposals (each, a “Proposal” and, together, the “Proposals”) and keep it for future reference.

QUESTIONS AND ANSWERS

Q. Why are you sending me this information?

A. You are receiving these proxy materials because on May 9,15, 2023 (the “Record Date”), you owned shares of VidentDistillate Small/Mid Cash Flow ETF (“DSMC”), Distillate U.S. Bond Strategy ETF™Fundamental Stability & Value ETF (“VBND”), Vident U.S. Equity Strategy ETF™ (“VUSE”), Vident International Equity Strategy ETF™ (“VIDI”DSTL”), and/or U.S. Diversified Real EstateDistillate International Fundamental Stability & Value ETF (“PPTY”DSTX”) (each, a “Fund,”“Fund” and, collectively, the “Funds”) and, as a result, you have the right to vote on the ProposalProposals and are entitled to be present at and to vote at the Special Meeting. Each share of a Fund is entitled to one vote on the applicable Proposal.

Q. What isare the ProposalProposals being considered at the Special Meeting?

A. You are being asked to vote on the following proposal(s):proposals:

PROPOSAL 1: For shareholders of each PROPOSAL 2: For shareholders of each Fund, separately, to approve a “manager of managers” arrangement that would grant the applicable Fund and the Adviser greater flexibility to change sub-advisory arrangements without shareholder approval, subject to prior approval by the Trust’s Board of Trustees. No increase in shareholder fees or expenses is being proposed. |

Q. Will theeither Proposal affect the investments made by the Funds?

A. No. Approval of the ProposalProposals by each Fund’s shareholders will not have any effect on the relevant Fund’s investment policies, strategies, and risks.

Q. Will the ProposalProposals result in any change in the fees or expenses payable by the Funds?

A. No. Approval of the ProposalProposals by each Fund’s shareholders will not affect the fees or expenses payable by each Fund. If the New AdvisorySub-Advisory Agreement is approved by each Fund’s shareholders, each Fund will pay VA a managementthe fee equalpaid to the management fee currently being paid by such Fund to VA.Adviser will not change as a result of the shareholder vote.

Q. Why am I being asked to approve a new investment advisorysub-advisory agreement with VA?

A. Pursuant to a purchase agreement signed on March 24, 2023, Vident Capital Holdings, LLC, a subsidiary of MM VAM, LLC(“LLC (“VA Holdings”), is expected to acquire a majority interest in VA on or around June 30, 2023 (the “Transaction”). MM VAM, LLC is an entity controlled by Casey Crawford. As of the Closing Date, Mr. Crawford will effectively control VA. The Transaction is expected to be completed on or around June 30, 2023 (the “Closing Date”), subject to the satisfaction of customary closing conditions, including obtaining necessary Fund and client consents and receipt of customary regulatory approvals. The Transaction will constitute an “assignment” under the Investment Company Act of 1940, as amended (the “1940 Act”), which will result in the automatic termination of the current investment advisorysub-advisory agreement between the Trust, on behalf of the Funds, and VA and the current investment sub-advisory agreement among the Trust, on behalf of the Funds, VAAdviser and Vident Investment Advisory, LLC (“VIA”) (the “Current Sub-Advisory Agreement”). On the Closing Date, VIA will no longer serve as sub-adviser to the Funds and VA will perform all portfolio management and trading responsibilitysub-advisory responsibilities on behalf of the Funds.Funds, which were previously provided by VIA.

To enable VA to continue servingtake over from VIA to serve as investment advisersub-adviser to the Funds after the close of the Transaction, at a meeting of the Board held on April 20, 2023, the Board, including a majority of the Trustees who are not “interested persons” (as that term is defined in the 1940 Act (the “Independent Trustees”), approved a new investment advisorysub-advisory agreement between the Trust, on behalf of the Funds,Adviser and the Adviser.VA. Under the 1940 Act, the approval of the Funds’ new investment advisorysub-advisory agreement also requires the affirmative vote of a “majority of the outstanding voting securities” of each Fund.

If a Fund’s shareholders approve the New AdvisorySub-Advisory Agreement, VA will continue to serve as the Funds’ investment adviser effective upon the closing of the Transaction.

Q. Why am I not being asked to approve a new investment sub-advisory agreement with VIA?

A. At the Closing Date, VIA will seek to move all its current personnel and clients to VA and wind down operations. For this reason, you are not being asked to approve a new sub-advisory agreement with VIA.

Q. Will there be any changes in the sub-advisory services provided to the Funds under the new agreements?agreement?

A. Yes. UnderNo. It is not anticipated that the Transaction or the approval of the New AdvisorySub-Advisory Agreement not only will VA continue to have overall responsibility for the general management and administrationimpact Fund shareholders. The terms of the Funds, but itNew Sub-Advisory Agreement are identical to the Current Sub-Advisory Agreement except for date of effectiveness, term and the fact that the new entity is VA. The advisory fee rate charged will also assume all ofremain the responsibilities that were previously assumedsame as under the Current Sub-Advisory Agreement and the Interim Sub-Advisory Agreement (defined below). If approved by VIA (e.g., day-to-day portfolio managementshareholders, the New Sub-Advisory Agreement will have an initial two-year term and services such as buying and selling portfolio securities for each Fund).

will be subject to annual renewal thereafter.

Q. Will there be any changes to the portfolio management team for any of the Funds?

A. No. The portfolio management team for each Fund will not change if shareholders of a Fund approve the Proposal.Proposals.

Q. Why am I being asked to vote on Proposal 2?

A. The Trust has requested exemptive relief from the Securities and Exchange Commission (the “SEC”) that would provide the Adviser with the flexibility to enter into and materially amend sub-advisory agreements with affiliated or unaffiliated sub-advisers, with the approval of the Board, but without shareholder approval. This exemptive relief would allow the Funds to avoid the costs and delays associated with holding a shareholder meeting. This relief is referred to as “manager of managers” relief. As a condition of the exemptive relief, a Fund would be required to receive shareholder approval to rely on the manager of managers relief prior to first use.

The proposed “manager of managers” arrangement will empower the Board, on behalf of the Funds, to approve a new sub-adviser, or change an existing sub-adviser, without a proxy solicitation. Under the arrangement, shareholders will receive substantially the same information about a sub-adviser change as they would have received if they had received voting materials for the change. This information will be delivered to shareholders within 90 days after the change. The Board, including a majority of the Independent Trustees, is required to approve any agreement with a new sub-adviser or any change in an existing sub-adviser’s agreement.

Q. Would the Funds have to pay more fees or expenses with the “manager of managers” structure?

A. No. If a new sub-adviser charges a higher fee than its predecessor (or if an existing sub-adviser increases its fee), and the Board, including a majority of Independent Trustees, approves the higher sub-advisory fee, the Adviser would not be permitted to pass these costs on to the Funds without first obtaining shareholder approval via proxy solicitation. Therefore, a new sub-adviser may charge a higher fee than its predecessor (or an existing sub-adviser may increase its fee), subject to Board approval, without obtaining shareholder approval, as long as the increase in sub-advisory fees does not result in an increase in the Fund’s overall management fee.

Q. What will happen if a Fund’sFund shareholders do not approve the Proposal?Proposal 1?

A. The Transaction is subject to customary closing conditions. One condition is that VA must obtain the approval of a certain percentage of client accounts for closing to take place. As closing is not predicated on a single fund it is possible that the Transaction could close without a Funds approval. In the event a Fund is not able to obtain shareholder approval prior to the Closing Date, the Board, including a majority of the Independent Trustees, also approved an interim investment advisorysub-advisory agreement (the “Interim AdvisorySub-Advisory Agreement”) between the Trust on behalf of the FundAdviser and VA, so that VA could continuecan take over for VIA in managing the Fund after the change of control. Pursuant to Rule 15a‑4 under the 1940 Act, the Interim Investment AdvisorySub-Advisory Agreement will allow the Fund an additional 150 days to obtain shareholder approval of the New AdvisorySub-Advisory Agreement. The terms of the Interim Investment AdvisorySub-Advisory Agreement are substantially identical to the terms of the prior investment advisory agreement and prior sub-advisory agreement,Current Sub-Advisory Agreement, except for the term and escrow provisions, and the additionprovisions. Shareholder approval of the sub-advisory services set forth in the prior sub-advisory agreement. Additionally, under the Interim Investment Advisory Agreement, management fees earned by VA would be held in an interest-bearing escrow account until shareholders approve the New Advisory Agreement with VA with respect to its Fund. Shareholder approvalProposal 1 would need to be obtained within 150 days from the Closing Date.

If a Fund’s shareholders do not approve the New Investment AdvisorySub-Advisory Agreement, then the Board will have to consider other alternatives for the Fund upon the expiration of the prior advisory agreementCurrent Sub-Advisory Agreement and Interim Investment AdvisorySub-Advisory Agreement. As a result of the Transaction the Current Advisory and Sub-Advisory AgreementThe Board will automatically terminate at the close of the Transaction. In such a situation, the Board would take such action as it deems necessary and in the best interests of each Fund and its respective shareholders, which may include further solicitation of that Fund’s shareholders with respect to the Proposal or solicitation of the approval of a different Proposal.

Q. What will happen if Fund shareholders do not approve Proposal 2?

A. If a Fund’s shareholders do not approve Proposal 2, then the Board will take such action as it deems necessary and in the best interests of each Fund and its respective shareholders, which may include further solicitation of that Fund’s shareholders with respect to the Proposal or solicitation of the liquidationapproval of one or more Funds.a different Proposal.

Q. How does the Board recommend that I vote in connection with the Proposal?Proposals?

A. The Board recommends that you vote “FOR” the approval of the ProposalProposals described in the Proxy Statement.

OTHER MATTERS

Q. Will my Fund(s) pay for this proxy solicitation?

A. No. VA or its affiliates will pay for the costs of this proxy solicitation, including the printing and mailing of the Proxy Statement and related materials. Under the terms of the Transaction, VA Holdings has agreed to reimburse VA for certain expenses related to obtaining new advisory agreements for each Fund.

Q. How can I vote my shares?

A. For your convenience, there are several ways you can vote:

By Mail: Complete, sign and return the enclosed proxy card(s) in the enclosed self-addressed, postage-paid envelope;

By Telephone: Call the number printed on the enclosed proxy card(s) and use the control number provided;

By Internet: Access the website address printed on the enclosed proxy card(s) and use the control number provided; or

In Person: Attend the Special Meeting as described in the Proxy Statement.

We intend to hold the Special Meeting in person. However, we are sensitive to the public health and travel concerns our shareholders may have and recommendations that public health officials may issue in light of the evolving COVID-19 pandemic. As a result, we may impose additional procedures or limitations on Special Meeting attendees or may decide to hold the Special Meeting in a different location or solely by means of remote communication. We plan to announce any such updates on our proxy website www.videntam.com,https://proxyvotinginfo.com/p/distillate2023, and we encourage you to check this website prior to the Special Meeting if you plan to attend. We also encourage you to consider your options to vote by internet, telephone, or mail, as discussed above, in advance of the Special Meeting in the event that, as of June 9,30, 2023, in-person attendance at the Special Meeting is either prohibited under a federal, state, or local order or contrary to the advice of public health care officials.

Q. How may I revoke my proxy?

A. Any proxy may be revoked at any time prior to its use by written notification received by the Trust’s Secretary, by the execution and delivery of a later-dated proxy, or by attending the Special Meeting and voting in person. Shareholders whose shares are held in “street name” through their broker will need to obtain a legal proxy from their broker and present it at the Special Meeting in order to vote in person. Any letter of revocation or later-dated proxy must be received by the appropriate Fund prior to the Special Meeting and must indicate your name and account number to be effective. Proxies voted by telephone or Internet may be revoked at any time before they are voted at the Special Meeting in the same manner that proxies voted by mail may be revoked.

Q. What vote is required to approve the Proposal?Proposals?

A. The New Advisory Agreement must be approved by a voteApproval of each proposal requires a majority of the outstanding voting securities of a Fund. The “vote of the majority of the outstanding voting securities” is defined in the 1940 Act as the lesser of the vote of (i) 67% or more of the voting securities of the applicable Fund present at the Special Meeting or represented by proxy if holders of more than 50% of such Fund’s outstanding voting securities are present or represented by proxy; or (ii) more than 50% of the outstanding voting securities of the applicable Fund.

Q. Where can I obtain additional information about this Proxy Statement?

A. If you need any assistance or have any questions regarding the ProposalProposals or how to vote your shares, please call our proxy solicitor, Morrow Sodali Fund Solutions, LLC, at 866-839-1852. Representatives are available to assist you Monday through Friday, 9:00 a.m. to 10:00 p.m. Eastern time.

each a series of ETF Series Solutions

615 East Michigan Street

Milwaukee, Wisconsin 53202

PROXY STATEMENT |

This Proxy Statement is being furnished to the shareholders of VidentDistillate Small/Mid Cash Flow ETF, Distillate U.S. Bond Strategy ETF™, Vident U.S. Equity Strategy ETF™, VidentFundamental Stability & Value ETF, and Distillate International Equity Strategy ETF™, and U.S. Diversified Real EstateFundamental Stability & Value ETF (each, a “Fund,”“Fund” and, collectively, the “Funds”), each a series of ETF Series Solutions (the “Trust”), an open-end management investment company, on behalf of the Trust’s Board of Trustees (the “Board”) in connection with each Fund’s solicitation of its shareholders’ proxies for use at a special meeting of shareholders of the Funds (the “Special Meeting”) to be held on June 9,30, 2023, at 11:00[TIME] a.m. Central time at the offices of the Funds’ administrator, U.S. Bank Global Fund Services, 615 East Michigan Street, Milwaukee, Wisconsin 53202, for the purposes set forth below and in the accompanying Notice of Special Meeting.

Shareholders of record at the close of business on the record date, established as May 9,15, 2023 (the “Record Date”), are entitled to notice of, and to vote at, the Special Meeting. The approximate mailing date of this Proxy Statement and the enclosed proxy card(s) to shareholders is May 16, 2023.[MAILING DATE, 2023]. The Special Meeting will be held to obtain shareholder approval for the following Proposal (theProposals (each, a “Proposal” and, together, the “Proposals”):

PROPOSAL 1:For shareholders of each |

PROPOSAL 2:For shareholders of each Fund, separately, to approve a “manager of managers” arrangement that would grant the applicable Fund and the Adviser greater flexibility to change sub-advisory arrangements without shareholder approval, subject to prior approval by the Trust’s Board of Trustees. No increase in shareholder fees or expenses is being proposed.

At your request, the Trust will send you a free copy of the most recent audited annual report for the relevant Fund or its current prospectus and statement of additional information (“SAI”). Please call the Funds at 1-800-617-0004 or write to the Distillate Funds, c/o U.S. Bank Global Fund Services, P.O. Box 701, Milwaukee, Wisconsin 53201-0701, to request an annual report, prospectus, or SAI, or with any questions you may have relating to this Proxy Statement.

Background. VA, Vident Investment Advisory, LLC (“VIA”), the Funds’ current investment adviser,sub-adviser, located at 1125 Sanctuary Parkway, Suite 515, Alpharetta, Georgia 30009, is an investment adviser registered with the U.S. Securities and Exchange Commission (“SEC”) and has provided investment advisory services.Pursuant to the Funds since 2019.

VA, an affiliate of VIA, was formed in 2016 and commenced operations and registered with the SEC as an investment adviser in 2019 and is a wholly-owned subsidiary of Vident Financial, LLC (“Vident Financial”). VIA was formed in 2014 and provides investment advisory services to ETFs, including the Funds. VIA is also a wholly-owned subsidiary of Vident Financial. Vident Financial was formed in 2013 to develop and license investment market solutions (indices and funds) based on strategies that combine sophisticated risk-balancing methodologies, economic freedom metrics, valuation, and investor behavior. Vident Financial is a wholly-owned subsidiary of the Vident Investors’ Oversight Trust. Vince L. Birley, Mohammad Baki, and W. Baker Crow serve as the trustees of the Vident Investors’ Oversight Trust.

Pursuant to a purchase agreement signed on March 24, 2023, Vident Capital Holdings, LLC, a subsidiary of MM VAM, LLC is expected to acquire VA (the “Transaction”). MM VAM, LLC is an entity controlled by Casey Crawford. The Transaction is expected to be completed on or around June 30, 2023 (the “Closing Date”), subject to the satisfaction of customary closing conditions, including obtaining certain Fund and client consents and receipt of customary regulatory approvals. As of the Closing Date, Mr. Crawford will effectively control VA. Pursuant to the Investment Company Act of 1940, as amended (the “1940 Act”), the investment advisory agreement between the Trust, on behalf of the Funds and VA (the “Current Advisory Agreement”)Current Sub-Advisory Agreement will automatically terminate on the Closing Date. The Current Sub-Advisory Agreement among the Adviser, VIA, and the Trust, on behalf of the Funds (the “Current VIA Sub-Advisory Agreement”) will also automatically terminate on the Closing Date.

1

At a meeting of the Board, held on April 20, 2023 (the “Meeting”), the Adviser requested, and the Board, including a majority of the Trustees who are not interested persons of the Trust (as defined by the 1940 Act) (the “Independent Trustees”), approved (i) a new investment advisorysub-advisory agreement between the Trust, on behalf of the Funds,Adviser and the AdviserVA (the “New AdvisorySub-Advisory Agreement”); and (ii) an interim advisorysub-advisory agreement between the Trust, on behalf of the Funds,Adviser and the AdviserVA (the “Interim Sub-Advisory Agreement”).

Under the 1940 Act, the approval of the New Advisory Agreementeach Proposal with respect to a Fund requires the affirmative vote of a “majority of the outstanding voting securities” of each applicablesuch Fund. The “vote of the holders of a majority of the outstanding voting securities” is defined in the 1940 Act as the lesser of the vote of shareholders holding (i) 67% or more of the voting securities of a Fund present at the Special Meeting or represented by proxy if holders of more than 50% of such Fund’s outstanding voting securities are present or represented by proxy; or (ii) more than 50% of the outstanding voting securities of a Fund. Shareholders will have equal voting rights (i.e., one vote per share). Abstentions and “broker non-votes” (i.e., shares held by brokers or nominees as to which (i) instructions have not been received from the beneficial owner or the persons entitled to vote and (ii) the broker does not have discretionary voting power on a particular matter) will have the same effect as votes against the Proposal.Proposals. Accordingly, you are being asked to approve theboth Proposal 1 (the New Advisory Agreement.Sub-Advisory Agreement) and Proposal 2 (the manager of managers arrangement).

The Board believes the Proposal isProposals are in the best interests of each Fund and its shareholders and recommends that you vote “FOR” the Proposal. Proposals. Importantly, approval of the ProposalProposals will not result in any increase in shareholder fees or expenses.

At the Meeting, the Board, including the majority of the Independent Trustees, determined that the approval of VA to continue servingserve as the Funds’ investment adviser, and assume all duties of VIA, the current sub-adviser was in the best interest of each Fund and its respective shareholders, approved the New AdvisorySub-Advisory Agreement, and recommended that it be submitted to the Funds’each Fund’s shareholders for approval.

The Current AdvisorySub-Advisory Agreement was most recently approved by the Board, including a majority of the Independent Trustees, on January 11-12, 2023,April 20-21, 2022, with respect to DSTL and DSTX, and on July 21, 2022, with respect to DSMC, and by the shareholdersinitial shareholder of each Fund on March 28, 2019.at inception.

The Current Advisory Agreement and Current Sub-Advisory Agreement are collectivelyis materially identical to the New AdvisorySub-Advisory Agreement in all material respects, except for theirthe effective and termination dates.

If the Proposal is approved by a Fund’s shareholders prior to the close of the Transaction, the New AdvisorySub-Advisory Agreement is expected to become effective upon the closing of the Transaction. The Transaction is subject to customary closing conditions, including obtainingconditions. One condition is that VA must obtain the approval of a certain numberpercentage of client accounts for closing to take place. As closing is not predicated on a single fund it is possible that the new agreements by the Board of Trustees of the Trust and shareholders of each applicable Fund.Transaction could close without a Funds approval. If the shareholders of a Fund do not approve the Proposal at the Special Meeting, it is possible that a condition to the closing of the Transaction will not be satisfied and VA will continue to serve as the investment adviser to each Fund and VIA will continue to serve as the investment sub-adviser to each Fund pursuant to the Current Advisory Agreement and Current Sub-Advisory Agreement, respectively.Agreement. Accordingly, if the Proposal is not approved by a Fund’s shareholders, as applicable, at the Special Meeting, the Board will take such action as it deems necessary and in the best interests of the Fund and its shareholders, which may include further solicitation of a Fund’s shareholders with respect to the Proposal or solicitation of the approval of a different Proposal, or the liquidation of one or more Funds.Proposal.

Summary of the New AdvisorySub-Advisory Agreement. A copy of the form of New AdvisorySub-Advisory Agreement is attached to this Proxy Statement as Exhibit A. The following description of the material terms of the New AdvisorySub-Advisory Agreement is only a summary and is qualified in its entirety by reference to Exhibit A. References to the “Current Agreements” is inclusive of the Current Advisory Agreement and Current Sub-Advisory Agreement.

Duration and Termination. The New AdvisorySub-Advisory Agreement, like the Current AdvisorySub-Advisory Agreement, will remain in effect for an initial period of two years, unless sooner terminated. After the initial two-year period, continuation of the New AdvisorySub-Advisory Agreement from year to year is subject to annual approval by the Board, including at least a majority of the Independent Trustees.

Both the Current AdvisorySub-Advisory Agreement and the New AdvisorySub-Advisory Agreement (each, a “Sub-Advisory Agreement”) may be terminated without penalty (i) by vote of a majority of the Board, (ii) by vote of a majority of the outstanding voting securities of the Fund, or (iii) by the Adviser, in each case, upon one-hundred twenty (120)sixty (60) days’ written notice to VIA and VA, respectively (each, a “Sub-Adviser”). In addition, each Sub-Advisory Agreement may be terminated without penalty by the Sub-Adviser upon ninety (90) days’ written notice to the Trust.Adviser and the Board.

Sub-Advisory Services. The Current AdvisoryEach Sub-Advisory Agreement and the New Advisory Agreement requirerequires that the AdviserSub-Adviser regularly provide each Fund with investment research, advice and supervision and continuously furnish an investment program for the Funds, consistent with the respective investment objectives and policies of each Fund. Under the Current Agreements, the Adviser is responsible for determining each Fund’s assets to be purchased or sold by the Fund and has the authority to select and retain a sub-adviser to perform some or all of the services for which the Adviser is responsible. In addition, the New Advisory Agreement requires the Adviser to perform services set forth in the Current Sub-Advisory Agreement, such as determining the portfolio assets to be purchased or sold by a Fund, in accordance with such Fund’s investment objective, guidelines, policies and restrictions, and selecting broker-dealers to execute purchase and sale transactions, subject to the supervision of the Adviser and the Board.

| Name of Fund | Management Fee | Advisory Fees paid by each Fund to the Adviser | Advisory Fees Paid by each Fund to the Adviser |

| Vident U.S. Bond Strategy ETF™ | 0.41% | 0.41% | $1,626,266 |

| Vident U.S. Equity Strategy ETF™ | 0.50% | 0.50% | $2,285,277 |

| Vident International Equity Strategy ETF™ | 0.61% | 0.61% | $2,549,776 |

| U.S. Diversified Real Estate ETF | 0.53% | 0.49% | $631,6801 |

| Name of Fund | Sub-Advisory Fee | Minimum Fee | Fee Paid to Sub-Adviser |

Distillate Small/Mid Cash Flow ETF | 0.030% on the first $250,000,000 0.025% on the next $250,000,000 0.020% on net assets in excess of $500,000,000 | $20,000 | NA1 |

Distillate U.S. Fundamental Stability & Value ETF | 0.030% on the first $250,000,000 0.025% on the next $250,000,000 0.020% on net assets in excess of $500,000,000 | $25,000 | $2,527,050 |

Distillate International Fundamental Stability & Value ETF | 0.040% on the first $250,000,000 0.035% on the next $250,000,000 0.030% on net assets in excess of $500,000,000 | $12,500 | $130,080 |

1Vident Advisory, LLC contractually agreedThe Fund’s inception date was October 5, 2022 so no fees were paid to waive four basis points (0.04%) of its unified management fee until June 30, 2023. The fee waiver agreement will automatically terminate on June 30, 2023. Without the fee waiver total fees would have been $683,246.Sub-Adviser during the prior fiscal year.

Brokerage Policies. The Current Agreements andEach Sub-Advisory Agreement authorizes the New Advisory Agreement authorize the Funds’ AdviserSub-Adviser to select the brokers or dealers that will execute the purchases and sales of securities of the Funds and directdirects the AdviserSub-Adviser to seek for each Fund the most favorable execution and net price available under the circumstances. The AdviserSub-Adviser may cause a Fund to pay a broker a commission more than that which another broker might have charged for effecting the same transaction, in recognition of the value of the brokerage and research and other services provided by the broker to the Adviser.Sub-Adviser.

The table below shows brokerage commissions paid in the aggregate amount by each Fund for its most recent fiscal year (ended August 31, 2022 for VBND, VUSE, and VIDI and ended February 28, 2023 for PPTY)September 30, 2022).

| Name of Fund | FYE $ |

$ | |

| $ | |

| $ | |

1. | The inception date of Distillate Small/Mid Cash Flow ETF was October 5, 2022. |

During its most recent fiscal year no Fund paid brokerage commissions to any registered broker-dealer affiliates of the Funds or the Adviser. The Funds did not holdNo Fund held any securities of “regular broker dealers” as of its most recent fiscal year end.

Payment of Expenses. BothUnder each Sub-Advisory Agreement, the Current Advisory Agreement and the New Advisory Agreement provide that the Adviser will paySub-Adviser agrees to bear all of the costs andits expenses incurred by it in connection with the advisoryperformance of its services provided forunder the Funds. The Adviser will not be requiredSub-Advisory Agreement, including provision of personnel, office space, and equipment reasonably necessary to pay the costs and expenses associated with purchasing securities, commodities, and other investments for the Funds (including brokerage commissions and other transaction or custodial charges). Additionally, both the Current Advisory Agreement and the New Advisory Agreement state that the Adviser agrees to pay all expenses incurred by the Funds except for the fee paidprovide sub-advisory services to the Adviser pursuant to this Agreement, interest charges on any borrowings, dividends and other expenses on securities sold short, taxes, brokerage commissions and other expenses incurred in placing orders for the purchase and sale of securities and other investment instruments, acquired fund fees and expenses, accrued deferred tax liability, extraordinary expenses, and distribution fees and expenses paid by the Trust under any distribution plan adopted pursuant to Rule 12b-1 under the 1940 Act. Funds.

Other Provisions. BothEach Sub-Advisory Agreement provides that in the Current Advisory Agreement and the New Advisory Agreement provide that the Adviser shall indemnify and hold harmless the Trust and all affiliated persons (within the meaningabsence of Section 2(a)(3) of the 1940 Act) and all controlling persons (as described in Section 15 of the Securities Act of 1933, as amended (the “1933 Act”)) thereof (collectively, the “Trust Indemnitees”) against any and all losses, claims, damages, liabilities or litigation to the extent that a Trust Indemnitee incurs actual losses, damages, or liabilities (including reasonable legal and other expenses) by reason of or arising out of the Adviser’s willful misfeasance, fraud, bad faith, or gross negligence in the performance of its duties, underor by reason of the agreement or its reckless disregard of its obligations and duties under the agreement. Sub-Advisory Agreement on the part of the Sub-Adviser, the Adviser shall indemnify and hold harmless the Sub-Adviser and its affiliates from and against any and all claims, losses, liabilities or damages arising from or in connection with the Sub-Advisory Agreement. In addition, each Sub-Advisory Agreement provides that the Sub-Adviser shall indemnify and hold harmless the Adviser, the Trust, and their affiliates from and against any and all claims, losses, liabilities or damages arising from or in connection with the Sub-Adviser’s obligations under the Sub-Advisory Agreement resulting from or relating to the Sub-Adviser’s own willful misfeasance, fraud, bad faith, or gross negligence in the performance of its duties, or by reason of the reckless disregard of its duties under the Sub-Advisory Agreement.

3

Executive Officers and Directors of VA. Information regarding the principal executive officers and directors of VA is set forth below. The address of VA and its executive officers and directors is 1125 Sanctuary Parkway, Suite 515, Alpharetta, Georgia 30009. The following individuals are the executive officers and directors of VA:

| Name | Position with VA |

| Deborah Kimery | Chief Executive Officer |

| Erik Olsen | Chief Compliance Officer |

No Trustee or officer of the Trust currently holds any position with VA or its affiliated persons. No Trustee or officer of the Trust holds any position with Vident Capital Holdings, LLC or its affiliated persons.

Recommendation of the Board of Trustees. The Board believes that the terms and conditions of the New AdvisorySub-Advisory Agreement are fair to, and in the best interests of, each Fund and its shareholders. The Board believes that, upon shareholder approval of the Proposal, the AdviserVA (the “Sub-Adviser”) will provide at least the same level of services that it and its affiliate VIA currently provideprovides each Fund under the Current Agreements.Sub-Advisory Agreement. The Board was presented with information demonstrating that the New AdvisorySub-Advisory Agreement would enable the Funds’ shareholders to continue to obtain quality services at a cost that is fair and reasonable. At the Meeting, the Board, including all of the Independent Trustees, approved the New AdvisorySub-Advisory Agreement and recommends that shareholders of each Fund approve the Proposal.

In considering the New AdvisorySub-Advisory Agreement, the Board focused on the effect that the Transaction could be expected to have on the Adviser’sSub-Adviser’s business and operations as they relate to the Funds and also took into consideration (i) the nature, extent, and quality of the services provided by VIA and to be provided by VA; (ii) the historical performance of each Fund; (iii) the cost of the services provided and the profits realized by VAVIA or its affiliates from services rendered to the Funds as well as the estimated cost of the services to be provided by its affiliate VA and the profits expected to be realized by VA from providing such services, including any other financial benefits enjoyed by VIA, or that will be enjoyed by VA, or itstheir affiliates; (iv) comparative fee and expense data for the Funds and other investment companies with similar investment objectives, including a report prepared by Barrington Partners, an independent third party, that compares each Fund’s investment performance, fees and expenses to relevant market benchmarks and peer groups (the “Barrington Report”); (v) the extent to which any economies of scale realized by VIA or VA in connection with its services to the Funds are, or will be, shared with Fund shareholders; and (vi) other factors the Board deemed to be relevant.

The Board also considered that the Adviser and its affiliate VIA, along with other service providers of the Funds, had provided written and oral updates on the firm over the course of the year with respect to its role as investment adviser and sub-adviser to the Funds, and the Board considered that information alongside the written materials presented at the Meeting, as well as the quarterly Board meeting held on April 5-6, 2023, in its consideration of whether the New AdvisorySub-Advisory Agreement should be approved. In addition, the Board took into consideration performance and due diligence information related to VA,VIA, including the Barrington Report,Reports, that was provided to the Board in advance of its (i) annual review of the Funds’ Current AdvisorySub-Advisory Agreement, with respect to DSTL and DSTX, at its January 11-12, 2023 quarterly meeting.meeting on April 20-21, 2022, and (ii) initial approval of the Current Sub-Advisory Agreement, with respect to DSMC, at its quarterly meeting on July 21, 2022. At both the Meeting and the April 5-6 meeting, representatives from VA provided an overview of the Transaction and the effect it would have on the management of the Funds. Representatives from the AdviserSub-Adviser also provided an overview of the Funds’ strategies, the services to be provided to each Fund by the Adviser,Sub-Adviser, and additional information about the Adviser’sSub-Adviser’s personnel and business operations. Further, subsequent to the April 5-6 meeting, at the Board’s request, VA representatives provided additional information about the Transaction and discussed this information with Fund counsel prior to the Meeting. The Board then met with representatives of the AdviserSub-Adviser at the Meeting to further discuss the Transaction and the additional information the AdviserSub-Adviser had provided. The AdviserSub-Adviser confirmed that the Transaction would not result in changes to Funds’ fees and expenses or the nature, extent and quality of services provided to the Funds, including their day-to-day management, or the personnel providing these services. The Board then discussed the materials and the Adviser’sSub-Adviser’s oral presentations that the Board had received and any other information that the Board received at the Meeting and at prior meetings, and deliberated on the approval of the New AdvisorySub-Advisory Agreement in light of this information. In its deliberations, the Board did not identify any single piece of information discussed below that was all-important or controlling.

4

Nature, Extent, and Quality of Services Provided. The Trustees considered the scope of services provided under the New AdvisorySub-Advisory Agreement, noting that the AdviserVIA had provided and VA, its affiliate, would continue to provide investment management services to the Funds. The Trustees also considered that the services to be provided under the New AdvisorySub-Advisory Agreement were identical in all material respects to those services provided under the Current Agreements.Sub-Advisory Agreement. The Trustees noted that although VIA will cease to exist upon the close of the Transaction, VIA personnel will become AdviserVA personnel at such time and continue to provide services to the Funds on behalf of the Adviser.VA. In considering the nature, extent, and quality of the services provided by the Adviser,VIA, and to be provided by VA, the Board considered the quality of the Adviser’sSub-Adviser’s compliance program and past reports from the Trust’s Chief Compliance Officer (“CCO”) regarding the CCO’s review of the Adviser’sVIA’s compliance program. The Board also considered its previous experience with the AdviserVIA providing investment management services to the Funds. The Board noted that it had received a copy of the Adviser’sVA’s registration form and financial statements, as well as the Adviser’sVA’s response to a detailed series of questions that included, among other things, information about the Adviser’sVA’s decision-making process, the background and experience of the firm’s key personnel, and the firm’s compliance policies, marketing practices, and brokerage information.

The Board noted the responsibilities that the Sub-Adviser will have as each Fund’s investment sub-adviser, including: responsibility for the general management of the day-to-day investment and reinvestment of the assets of each Fund; determining the daily baskets of deposit securities and cash components; executing portfolio security trades for purchases and redemptions of each Fund’s shares conducted on a cash-in-lieu basis; oversight of general portfolio compliance with applicable securities laws, regulations, and investment restrictions; responsibility for quarterly reporting to the Board; and implementation of Board directives as they relate to the Funds. The Board also considered the Adviser’sSub-Adviser’s resources and capacity with respect to portfolio management, compliance, and operations given the number of funds for which it provides sub-advisory services. The Board also considered VA’s statements that the scope and quality of services provided to the Funds by the AdviserSub-Adviser would not diminish as a result of the Transaction.

Historical Performance. The Trustees next considered each Fund’s performance, except the recently launched DSMC, noting that itthey had recently undertaken a comprehensive review of such matters, with respect to DSTL and DSTX, at its January 11-12, 2023July 21, 2022 meeting. The Board observed that information regarding each Fund’s past investment performance, for periods ended September 30,March 31, 2022, had been included in the written materials previously provided to the Board, including the Barrington Report,Reports, which compared the performance results of each FundDSTL and DSTX with the returns of a group of ETFs selected by Barrington Partners as most comparable (the “Peer Group”) as well as with funds in each Fund’s Morningstar category – US Fund Real Estate, US Fund Intermediate Core-Plus Bond,Large Blend and US Fund Foreign Large Value, and US Fund Mid-Cap Value,Blend, respectively (each, a “Category Peer Group”). Additionally, at the Board’s request, the Adviser identified the funds the Adviser considered to be each Fund’s most direct competitors (each, a “Selected Peer Group”) and provided the Selected Peer Group’s performance results.

In addition to reviewing the results of the Barrington Reports, the Board noted that, for each applicable period ended September 30,December 31, 2022, each Fund’s performance on a gross of fees basis (i.e., excluding the effect of fees and expenses on Fund performance) was generally consistent with the performance ofDSTL outperformed its underlying index, indicating that each Fund tracked its underlying index closely and in an appropriate manner.

Cost of Services Provided and Economies of Scale. The Board observed that the Transaction would not result in an increase in the level of the advisorymanagement fee paid by each Fund to the Adviser.Adviser or the sub-advisory fee paid by the Adviser to the Sub-Adviser. In this regard, the Board reviewed each Fund’s fees and expenses, noting that the advisory fees to be paid to the AdviserVA for its services to the Funds under the New AdvisorySub-Advisory Agreement were identical to those inthe fees paid to VIA for its services under the Current AdvisorySub-Advisory Agreement. In addition, the Board took into consideration that the Adviser had charged, and would continue to charge, a “unified fee,” meaning each Fund pays no expenses other than the advisory fee and, if applicable, certain other costs such as interest, brokerage, acquired fund fees and expenses, extraordinary expenses, and, to the extent it is implemented, fees pursuant to a Distribution and/or Shareholder Servicing (12b‑1) Plan. The Board noted that the Adviser had been and would continue to be responsible for compensating the Trust’s other service providers and paying the Funds’ other expenses out of the Adviser’s own fee and resources.

The Board noted that each Fund’s net expense ratio was equal to its unified fee (described above), except that the U.S. Diversified Real Estate ETF has a fee waiver of four basis points and, as a result, its net expense ratio is less than its unified fee. The fee waiver would terminate effective June 30, 2023. The Board further took into consideration that it had recently evaluated a comparison of each Fund’s net expense ratio to its Peer Group and Category Peer Group, as shown in the Barrington Report, and its Selected Peer Group.

The Board then considered the Adviser’sSub-Adviser’s financial resources and information regarding the Adviser’sSub-Adviser’s ability to support its management of the Funds, and obligations under the unified fee arrangement, noting that the AdviserSub-Adviser had provided its financial statements for the Board’s review. The Board also evaluated the compensation and benefits received, and expected to be received, by the AdviserSub-Adviser from its relationship with the Funds, taking into account an analysis of the Adviser’sVIA’s profitability, and VA’s expected profitability, with respect to each Fund at various actual and projected Fund asset levels. In evaluating these matters, the Board considered the resources that would become available to the AdviserSub-Adviser as a result of the Transaction.

The Board expressed the view that it currently appeared that the AdviserSub-Adviser might realize economies of scale in managing the Funds as assets grow in size. The Board noted that shouldeach Fund’s sub-advisory fee rate schedule includes breakpoints that are initiated as Fund assets grow. The Board further noted that because each Fund pays the Adviser realizea unified fee, any benefits from such breakpoints in the sub-advisory fee schedule would accrue to the Adviser, rather than such Fund’s respective shareholders. Consequently, the Board determined that it would monitor fees as the Funds grow to determine whether economies of scale in the future, the Board would evaluate whether those economies were appropriatelybeing effectively shared with Fund shareholders, whether through the structureFunds and amount of the fee or by other means.their shareholders.

5

Conclusion. No single factor was determinative of the Board’s decision to approve the New AdvisorySub-Advisory Agreement; rather, the Board based its determination on the total mix of information available to it. Based on a consideration of all the factors in their totality, the Board, including the Independent Trustees, determined that the New AdvisorySub-Advisory Agreement, including the compensation payable under the agreement, was fair and reasonable to each Fund. The Board, including the Independent Trustees, determined that the approval of the New AdvisorySub-Advisory Agreement was in the best interests of each Fund and its shareholders.

You are being asked to approve a “manager of managers” arrangement that would permit the Proposal. All expenses associatedFunds and the Adviser to enter into, and materially amend, sub-advisory agreements with the Proposal will be borneany sub-advisers retained by the Adviser to manage all or its affiliates and nota portion of a Fund’s assets without obtaining shareholder approval, if the Board concludes that such an arrangement would be in the best interests of the Fund’s shareholders. The Board, including the Independent Trustees, has approved the use of a “manager of managers” arrangement by the Funds.Adviser with respect to each of the Funds, and any such arrangement utilized by the Funds would be subject to Board oversight and conditions imposed by the SEC in either a rule or an exemptive order, including the requirement that any sub-advisory agreement or material change to such agreement be approved by the Board (including a majority of the Independent Trustees). The Board believes that it is in the best interest of each Fund to afford the Adviser the flexibility to provide investment advisory services to each Fund through one or more sub-advisers. The Board also considered that Fund expenses will remain unaffected, and that any increases in the total fees paid by the Funds to the Adviser would still require shareholder approval.

If shareholders of a Fund approve Proposal 2, that Fund would be able to implement a “manager of managers” arrangement. Under a “manager of managers” arrangement, the Adviser and the Board of Trustees would be authorized to (1) engage new or additional affiliated or unaffiliated sub-advisers for the relevant Fund; (2) enter into and modify existing sub-advisory agreements for the relevant Fund with affiliated or unaffiliated sub-advisers; and (3) terminate and replace sub-advisers for a Fund with affiliated or unaffiliated sub-advisors without obtaining further approval of the Fund’s shareholders, provided the Board, including a majority of the Independent Trustees, has approved the new or amended agreement. The Board has determined to approve the proposed “manager of managers” arrangement for each Fund as this approach is expected to save a Fund the considerable cost and delay of seeking shareholder approval for any amendment or change to a Fund’s sub-advisory relationship. Each Fund would be authorized to disclose fees paid to sub-advisers on an aggregated basis rather than separately. Under the terms and conditions of the Order, the Funds would be subject to several conditions imposed by the SEC. For example, within 90 days of the hiring of a new sub-adviser, a Fund would be required to provide shareholders with (or electronic access to) an information statement containing information about the sub-adviser and the sub-advisory agreement, similar to that which would have been provided in a proxy statement seeking shareholder approval of such an agreement or change thereto.

THE BOARD RECOMMENDS THAT SHAREHOLDERS OF EACH FUND VOTE “FOR” THE PROPOSAL.PROPOSALS.

Importantly, approval of the Proposal will not result in any increase in shareholder fees or expenses.

OTHER INFORMATION

Section 15(f) of the 1940 Act. Because the Transaction may be considered to result in a change of control of the AdviserVIA under the 1940 Act resulting in the assignment of the Former AdvisoryCurrent Sub-Advisory Agreement, the AdviserSub-Adviser intends for the Transaction to come within the safe harbor provided by Section 15(f) of the 1940 Act, which permits an investment adviser of a registered investment company (or any affiliated persons of the investment adviser) to receive any amount or benefit in connection with a sale of an interest in the investment adviser that results in an assignment of an investment advisory contract, provided that the following two conditions are satisfied.satisfied:

First, an “unfair burden” may not be imposed on the investment company as a result of the sale of the interest, or any express or implied terms, conditions or understandings applicable to the sale of the interest. The term “unfair burden,” as defined in the 1940 Act, includes any arrangement during the two-year period following the transaction whereby the investment adviser (or predecessor or successor adviser), or any “interested person” of the adviser (as defined in the 1940 Act), receives or is entitled to receive any compensation, directly or indirectly, from the investment company or its security holders (other than fees for bona fide investment advisory or other services), or from any person in connection with the purchase or sale of securities or other property to, from or on behalf of the investment company (other than ordinary fees for bona fide principal underwriting services). The AdviserSub-Adviser has confirmed for the Board that the Transaction will not impose an unfair burden on the Fund within the meaning of Section 15(f) of the 1940 Act.

6

Second, during the three-year period following the Transaction, at least 75% of the members of the investment company’s board of trustees cannot be “interested persons” (as defined in the 1940 Act) of the sub-adviser (or predecessor sub-adviser). At the present time, 75% of the Trustees are classified as Independent Trustees; i.e., not interested persons of the Trust. The Board has committed to ensuring that at least 75% of the Trustees will not be “interested persons” of the Sub-Adviser for a period of three years after the Transaction.

Expenses Related to the Proposals. All expenses associated with the Proposals will be borne by VA or its affiliates and not by the Funds.

Record Date/Shareholders Entitled to Vote. Each Fund is a separate series, or portfolio, of the Trust, a Delaware statutory trust and registered investment company under the 1940 Act. The record holders of outstanding shares of each Fund are entitled to vote one vote per share (and a fractional vote per fractional share) on all matters presented at the Special Meeting with respect to each Fund, including the Proposal.Proposals.

Shareholders of each Fund at the close of business on May 9,15, 2023, the Record Date, will be entitled to be present and vote at the Special Meeting. As of the close of business on the Record Date, the following shares of each Fund were issued and outstanding:

Voting Proxies. You should read the entire Proxy Statement before voting. If you have any questions regarding the Proxy Statement, please call toll-free 866-839-1852. If you sign and return the accompanying proxy card, you may revoke it by giving written notice of such revocation to the Secretary of the Trust prior to the Special Meeting or by delivering a subsequently dated proxy card or by attending and voting at the Special Meeting in person. Proxies voted by telephone or internet may be revoked at any time before they are voted by proxy voting again through the website or toll-free number listed in the enclosed proxy card. Properly executed proxies will be voted, as you instruct, by the persons named in the accompanying proxy card. In the absence of such direction, however, the persons named in the accompanying proxy card intend to vote “FOR” the Proposal and may vote at their discretion with respect to other matters not now known to the Board that may be presented at the Special Meeting. Attendance by a shareholder at the Special Meeting does not, in itself, revoke a proxy.

If sufficient votes are not received for thea Proposal by the date of the Special Meeting, the Special Meeting may be adjourned with respect to such Proposal, once or more, by motion of the chair of the Special Meeting or by the vote of the holders of a majority of a Fund’s shares present at the Special Meeting in person or by proxy to permit further solicitation of proxies. If there is a vote to adjourn, persons named as proxies will vote all proxies in favor of adjournment that voted in favor of the ProposalProposals and vote against adjournment all proxies that voted against the Proposal.Proposals.

Quorum Required. Each Fund must have a quorum of shares represented at the Special Meeting, in person or by proxy, to take action on any matter relating to such Fund. Under the Trust’s Agreement and Declaration of Trust, as amended, a quorum is constituted by the presence in person or by proxy of at least one-third of the outstanding shares of a Fund entitled to vote at the Special Meeting.

Abstentions and broker non-votes (i.e., proxies from brokers or nominees indicating that they have not received instructions from the beneficial owners on an item for which the brokers or nominees do not have discretionary power to vote) will be treated as present for determining whether a quorum is present with respect to a particular matter. However, abstentions and broker non-votes will have the effect of a vote AGAINST the ProposalProposals and any other matter that requires the affirmative vote of a Fund’s outstanding shares for approval. Abstentions and broker non-votes will not be counted as voting on any other matter at the Special Meeting when the voting requirement is based on achieving a plurality or percentage of the “voting securities present.”

If a quorum is not present at the Special Meeting, or a quorum is present at the Special Meeting but sufficient votes to approve a Proposal is not received, the chair of the Special Meeting or the holders of a majority of a Fund’s shares present at the Special Meeting, in person or by proxy, may adjourn the Special Meeting with respect to such Proposal to permit further solicitation of proxies.

Required Vote. Approval of each Proposal requires the affirmative “vote of the holders of a majority of the outstanding voting securities” of a Fund. Under the 1940 Act, the “vote of the holders of a majority of the outstanding voting securities” means the affirmative vote of the lesser of (a) 67% or more of the shares of a Fund present or represented by proxy at the Special Meeting if the holders of more than 50% of the outstanding shares are present or represented by proxy at the Special Meeting, or (b) more than 50% of the outstanding shares of a Fund. If Proposal 1 is approved by a Fund’s shareholders prior to the close of the Transaction, the New Sub-Advisory Agreement is expected to become effective at the the closing of the Transaction. The Transaction is subject to customary closing conditions, including obtaining approval of a certain number of the new agreements by the Board of Trustees of the Trust and shareholders of each applicable Fund. If the shareholders of a Fund do not approve Proposal 1 at the Special Meeting, a condition to the closing of the Transaction may not be satisfied. Accordingly, if Proposal 1 is not approved by a Fund’s shareholders, as applicable, at the Special Meeting, the Board will take such action as it deems necessary and in the best interests of the Fund and its respective shareholders, which may include further solicitation of a Fund’s shareholders with respect to the Proposal or solicitation of the approval of a different proposal.

7

Method and Cost of Proxy Solicitation. Proxies will be solicited by the Trust, the Adviser, and/or Morrow Sodali Fund Solutions, LLC, a professional proxy solicitor (the “Proxy Solicitor”), primarily by mail. The solicitation may also include telephone, facsimile, electronic or oral communications by certain officers or employees of the Trust or the Adviser, none of whom will be paid for these services, or by the Proxy Solicitor. The Adviser will pay the costs of the Special Meeting and the expenses incurred in connection with the solicitation of proxies, including any expenses associated with the services of the Proxy Solicitor. The Trust may also request broker-dealer firms, custodians, nominees and fiduciaries to forward proxy materials to the beneficial owners of the shares of the Funds held of record by such persons. The estimated cost of the Proxy Solicitor for their services soliciting proxies from brokers, banks and other nominee holders is approximately $5,000 per Fund. The Adviser may reimburse such broker-dealer firms, custodians, nominees, and fiduciaries for their reasonable expenses incurred in connection with such proxy solicitation, including reasonable expenses in communicating with persons for whom they hold shares of a Fund.

Meeting Venue. We intend to hold the Special Meeting in person at the offices of U.S. Bank Global Fund Services, 615 East Michigan Street, Milwaukee, Wisconsin 53202. However, we are sensitive to the public health and travel concerns our shareholders may have and recommendations that public health officials may issue in light of the evolving COVID-19 pandemic. As a result, we may impose additional procedures or limitations on Special Meeting attendees or may decide to hold the Special Meeting in a different location or solely by means of remote communication. We plan to announce any such updates on our proxy website www.videntam.com,https://proxyvotinginfo.com/p/distillate2023, and we encourage you to check this website prior to the Special Meeting if you plan to attend. We also encourage you to consider your options to vote by internet, telephone, or mail, as discussed in the enclosed proxy card, in advance of the Special Meeting in the event that, as of June 9,30, 2023, in-person attendance at the Special Meeting is either prohibited under a federal, state, or local order or contrary to the advice of public health care officials.

Distributor, Administrator and Transfer Agent. The Funds’ distributor and principal underwriter is ALPSQuasar Distributors, Inc.,LLC, located at 1290 Broadway,111 East Kilbourn Avenue, Suite 1000, Denver, Colorado 80203.2200, Milwaukee, Wisconsin, 53202. U.S. Bancorp Fund Services, LLC, doing business as U.S. Bank Global Fund Services, located at 615 East Michigan Street, Milwaukee, Wisconsin 53202, serves as the Funds’ transfer agent and administrator.

Share Ownership. To the knowledge of the Trust’s management, as of the close of business on May 9,15, 2023, the officers and Trustees of the Trust, as a group, beneficially owned less than one percent of each Fund’s outstanding shares and less than one percent of the Trust’s outstanding shares. To the knowledge of the Trust’s management, as of the close of business on May 9,15, 2023, persons owning of record more than 5% of the outstanding shares of a Fund are as listed in the table below. The Trust believes that most of the shares referred to below were held by the persons indicated in accounts for their fiduciary, agency or custodial customers. Any shareholder listed below as owning 25% or more of the outstanding shares of a Fund may be presumed to “control” (as that term is defined in the 1940 Act) the applicable Fund. Shareholders controlling a Fund could have the ability to vote a majority of the shares of the applicable Fund on any matter requiring the approval of that Fund’s shareholders.

Name and Address | % Ownership | Type of Ownership |

Name and Address | % Ownership | Type of Ownership |

8

Distillate International Equity Strategy ETF™Fundamental Stability & Value ETF

Name and Address | % Ownership | Type of Ownership |

Reports to Shareholders. Copies of the Funds’ most recent annual and semi-annual reports may be requested without charge by writing to theDistillate Funds, c/o U.S. Bank Global Fund Services, 615 East Michigan Street, Milwaukee, Wisconsin 53202 or by calling toll-free 1-800-617-0004.

Other Matters to Come Before the Special Meeting. The Trust’s management does not know of any matters to be presented at the Special Meeting other than the ProposalProposals described above. If other business should properly come before the Special Meeting, the proxy holders will vote thereon in accordance with their best judgment.

Shareholder Proposal. The Agreement and Declaration of Trust, as amended, and the Amended and Restated By-laws of the Trust do not provide for annual meetings of shareholders, and the Trust does not currently intend to hold such meetings in the future. Shareholder proposal for inclusion in a proxy statement for any subsequent meeting of the Trust’s shareholders must be received by the Trust a reasonable period of time prior to any such meeting.

Householding. If possible, depending on shareholder registration and address information, and unless you have otherwise opted out, only one copy of this Proxy Statement will be sent to shareholders at the same address. However, each shareholder will receive separate proxy cards. If you would like to receive a separate copy of the Proxy Statement, please call 866-839-1852. If you currently receive multiple copies of Proxy Statements or shareholder reports and would like to request to receive a single copy of documents in the future, please call 1-800-617-0004 or write to the Funds, c/o U.S. Bank Global Fund Services at 615 East Michigan Street, Milwaukee, Wisconsin 53202.

Important Notice Regarding the Availability of Proxy Materials for the Special Meeting.

This Proxy Statement is available on the internet at https://proxyvotinginfo.com/p/videntetfs2023.distillate2023. Use the control number on your proxy card to vote by internet or by telephone. You may request a copy by mail (Vident(Distillate Funds, c/o U.S. Bank Global Fund Services, P.O. Box 701, Milwaukee, WI 53201-0701) or by telephone at 866-839-1852. You may also call for information on how to obtain directions to be able to attend the Special Meeting and vote in person.

9

EXHIBIT A

ETF SERIES SOLUTIONS

INVESTMENT ADVISORYSUB-ADVISORY AGREEMENT

with

VIDENT ADVISORY, LLC

This INVESTMENT ADVISORYSUB-ADVISORY AGREEMENT (the “Agreement”) is made as of this 6thXX day of April,XX, 2023 by and betweenamong DISTILLATE CAPITAL PARTNERS LLC, an Illinois limited liability company with its principal place of business at 53 West Jackson Blvd, Suite 530, Chicago, IL 60604 (the “Adviser”), ETF SERIES SOLUTIONS (the “Trust”), a Delaware statutory trust, and VIDENT ADVISORY, LLC, a Delaware limited liability company with its principal place of business located at 1125 Sanctuary Parkway, Suite 515, Alpharetta, GeorgiaGA 30009 (the “Adviser”“Sub-Adviser”).

W I T N E S S E T H

WHEREAS, the Trust is an open-end management investment company, and is registered as such under the Investment Company Act of 1940, as amended (the “1940 Act”); and

WHEREAS, the Trust desires to appointAdviser is registered as an investment adviser under the Investment Advisers Act of 1940 (the “Advisers Act”); and

WHEREAS, the Adviser has entered into an Investment Advisory Agreement dated July 12, 2018, as amended to serveadd additional series, with the Trust; and

WHEREAS, the Sub-Adviser is registered as thean investment adviser with respectunder the Investment Advisers Act of 1940 (the “Advisers Act”) and is engaged in the business of supplying investment advice as an independent contractor; and

WHEREAS, the Investment Advisory Agreement contemplates that the Adviser may appoint a sub-adviser to each seriesperform some or all of the Trust set forth on services for which the Adviser is responsible; and

WHEREAS, the Sub-Adviser is willing to furnish such services to the Adviser and each Fund listed in Schedule A to this Agreement (each a “Fund” and, collectively, the “Funds”);.

A G R E E M E N T

NOW, THEREFORE, in consideration of the mutual covenants and agreementsbenefits set out in this Agreement,forth herein, the Trust and the Adviserparties do hereby agree as follows:

1. a. Duties of the Sub-Adviser. Investment Description. Each Fund will investSubject to supervision and reinvest its assetsoversight of the Adviser and the Board of Trustees (the “Board”), and in accordance with the terms and conditions of the Agreement, the Sub-Adviser shall manage all of the securities and other assets of the Funds entrusted to it hereunder (the “Assets”), including the purchase, retention and disposition of the Assets, in accordance with the Funds’ respective investment objective(s),objectives, guidelines, policies and limitations specifiedrestrictions as stated in theeach Fund’s prospectus and statement of additional information, (the “Prospectus”) relating to such Fund filed with the SEC as part of the Trust’s Registration Statement on Form N-1A,currently in effect and as it may be periodically amended or supplemented from time to time (referred to collectively as the “Prospectus”), and subject to the following:

(a) The Sub-Adviser shall, subject to subparagraph (b), determine from time to time what Assets will be purchased, retained or sold by the Funds, and what portion of the Assets will be invested or held uninvested in accordancecash as is permissible.

10

(b) In the performance of its duties and obligations under this Agreement, the Sub-Adviser shall act in conformity with the Prospectus, the Statement of Additional Information, the written instructions and directions of the Adviser and of the Board, the terms and conditions of exemptive orders and no-action letters issuedrelief granted to the Trust as amended from time to time and provided to the Sub-Adviser and the Trust’s policies and procedures provided to the Sub-Adviser and will conform to and comply with the requirements of the 1940 Act, the Advisers Act, the Commodity Exchange Act, the Internal Revenue Code of 1986, as amended (the “Code”), and all other applicable federal and state laws and regulations, as each is amended from time to time.

(c) The Sub-Adviser shall determine the Assets to be purchased or sold by the SECFunds as provided in subparagraph (a) and will place orders with or through such persons, brokers or dealers to carry out the policy with respect to brokerage set forth in the Funds’ Prospectus or as the Board or the Adviser may direct in writing from time to time, in conformity with all federal securities laws. In executing Fund transactions and selecting brokers or dealers, the Sub-Adviser will use its staff.